The Origins of Market Madness and the Birth of Options

Financial markets have long been viewed as a realm of human emotion rather than scientific precision. Even the brilliant Isaac Newton (Isaac Newton) fell victim to the South Sea Bubble, famously remarking that he could calculate the motions of heavenly bodies but not the madness of people. This unpredictability stemmed from a lack of a standardized way to price risk, specifically in the form of options. An option is a contract giving the right, but not the obligation, to buy or sell an asset at a set price. This concept dates back to Thales of Miletus (Thales of Miletus) in 600 BC, who used options on olive presses to secure wealth based on his harvest predictions.

The modern understanding of these instruments began with Louis Bachelier (Louis Bachelier), who worked at the Paris Stock Exchange. He was the first to propose that stock prices follow a random walk, much like the movement of ball bearings on a Galton board. Bachelier realized that an efficient market is inherently unpredictable because if prices could be forecasted, traders would act immediately, shifting the price until the advantage disappeared. This insight laid the groundwork for the efficient market hypothesis.

| Option Type | Definition | Benefit |

|---|---|---|

| Call Option | Right to buy at a strike price | Profit from price increases with limited downside |

| Put Option | Right to sell at a strike price | Profit from price decreases or hedge against losses |

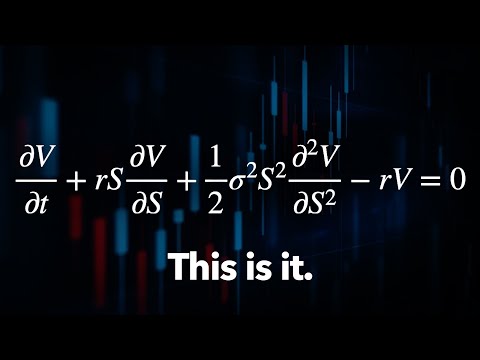

From Brownian Motion to the Mathematics of Uncertainty

Bachelier's work was ignored for decades, but it contained the same mathematical principles that Albert Einstein (Albert Einstein) used to solve the mystery of Brownian motion. Brownian motion refers to the random jittering of particles suspended in a fluid. Einstein proved that this movement was caused by trillions of invisible molecules colliding with the particles, providing definitive evidence for the existence of atoms. This connection between physics and finance is profound: both fields utilize the mathematics of stochastic calculus to describe systems governed by massive amounts of random interactions.

Edward Thorp (Edward Thorp), a physics professor and the inventor of card counting in blackjack, was the first to successfully bridge these worlds in the stock market. He applied his knowledge of probability and odds to identify mispriced warrants and options. Thorp's hedge fund delivered a 20% return every year for two decades by using what is known as dynamic hedging. This strategy involved balancing option positions with underlying stock to eliminate risk, essentially creating a synthetic insurance policy against market fluctuations.

ここからが大事な

ポイントです

具体例・注意点・明日から使えるヒントを整理しています。

✨無料閲覧で全文 + 図解の完全版を3日間いつでも読み返せる

あなたの好きな動画も、

1〜2分でAI要約

📚 お気に入り保存 + ✨ あなたの動画をAI要約

(無料登録10秒)

✏️ この記事で学べること

- ▸、 。 、 、 、 。

10秒で完了・パスワード作成不要